Don’t keep all your money in one bank account. It’s like not putting all your eggs in one basket.

Have different bank accounts with various banks, and make sure your bank accounts are not connected.

Think about having a separate/standalone bank account with a low balance, especially for online buying or selling and making payments to others.

In a recent parliamentary session, there was a suggestion that if a person falls victim to a scam, the person should be responsible for up to S$100 of the loss, with banks and telcos covering the rest.

This could lead some dishonest people to team up in cahoot with scammers to cheat the system and share the stolen money from scams.

However, no bank or telco will support this idea blindly. They might recover the scam losses by increasing bank charges for everyone, causing problems of common misery for all.

It seems like this proposal was not well thought out or conceived.

Was it just to gain popularity or voters’ attention? Be cautious and watch out for dishonest people – there are many charlatans around in town both in and outside Parliament, some could act as hidden advisors/consultants to the MPs.

==========

.

Forum: People may lower guard if liability for scam losses is limited to $100.

UPDATED 9 HOURS AGO on 16th Jan 2024 in ST Forum.

I agree with Aljunied GRC Member of Parliament Gerald Giam that stronger actions are needed to protect Singaporeans from scams, failing which the efforts of the Smart Nation movement may come to nought.

Victims of scams come in all ages. If young and technology-savvy Singaporeans are being conned, the older generation may be sceptical about using technology and hence will not be receptive to empowering themselves digitally.

Some of my older family members and friends have opted out of transactions involving digitalisation platforms and would rather be inconvenienced than be at risk of being scammed.

But I do not agree with Sengkang GRC MP Jamus Lim’s suggestion that victims of scams should bear no more than $100 to $500 in losses, with banks and telcos bearing the rest of the costs instead (S’pore launches new app guidelines to secure online transactions, Jan 10).

While I empathise with scammed victims on their losses, taking this step may only embolden the scammers who may feel less guilty about scamming victims.

Once we know the maximum amount that we will bear in a scam can be a mere $100, we may feel we do not need to be fully alert when we do a digital transaction.

We read reports that some victims of scams have bought or invested in products whose prices or claims are often too good to be true.

The financial institutions and telcos have no moral responsibility or obligation to compensate victims fully in such scams.

Family members must play an active role in advising their elderly parents or relatives to be extra alert when doing an online or digital transaction.

I too, like many Singaporeans, worry about being a victim of a scam. While I hope that banks and telcos will compensate me as much as possible if I am scammed, I know that the ultimate responsibility still rests with me.

Foo Sing Kheng.

\===========

.

No bank can eliminate greed and carelessness of their customers from becoming scam victims.

Do not keep all your eggs in one basket.

Open an indépendant standalone account with another bank not linked to your other bank accounts. Keep the balance in this standalone bank account very low, and use it for buying or selling things online, and for making payment to others.

Have a standalone credit card with another bank, and do not link it to any of your bank accounts.

The weakest link is the sim card, if it can be remotely stolen for use in another mobile phone without stealing your mobile phone or sim card.

============

.

.

At least 180 victims lost $2.6m in December to social media job offer scams

Victims are given a link to a fake TikTok website to complete advanced tasks, and are shown fake contracts to agree to. PHOTO: SINGAPORE POLICE FORCE

Sherlyn Sim

UPDATED 8 JAN 2024, 9:50 PM in Straits Times.

SINGAPORE – At least 180 people lost about $2.6 million in just one month after taking up fake job offers from conmen who later convinced them to transfer large sums of money in return for easy profits.

The victims got the unsolicited job offers from the scammers in December 2023 after being added to chat groups on messaging platforms like WhatsApp and Telegram.

They were then asked to get on social media platforms and perform specific tasks to earn a commission, the police said on Jan 8.

The tasks included following the TikTok or Instagram accounts of social media influencers, subscribing to YouTube channels and videos, or “liking” songs on Spotify.

“In some cases, scammers may also claim to represent TikTok or online communications and marketing companies when they approached victims with job offers.”

After completing the tasks, victims got a small commission, and were persuaded to complete more tasks in return for more money.

These tasks included getting the victims to create accounts on fake websites, and making them transfer large sums of money to bank accounts or cryptocurrency accounts provided by the scammers, with the promise of better returns.

In some cases, the conmen even offered victims fake employment contracts.

“Victims would only realise that they had been scammed when their website account showed a negative account balance, and they were told to pay additional funds in order to upgrade their accounts or when they failed to withdraw their earnings,” the statement said.

Victims said the conmen sent unsolicited WhatsApp or Telegram messages telling them they had won a prize and would get a commission when they completed tasks such as “following” an account on Instagram.

Victims were then added to chat groups where they got instructions to get active on social media sites or transfer cash under the pretence of investment opportunities.

The ruse involves victims getting unsolicited job offers from scammers after being added into chat groups. PHOTO: SINGAPORE POLICE FORCE

The police said members of the public need to guard against such scams by using the ScamShield app, enabling security features such as setting transaction limits for Internet banking, and setting up two-factor authentication.

Two-factor authentication is an extra layer of security that users can put in place before logging in to an online account or making an online transaction. It is usually a random code sent to a mobile device or a token.

Users should check if the offer is a scam by referring to official sources like the Anti-Scam Helpline or the Scam Alert website.

MORE ON THIS TOPIC

Single mum who lost $89k to a job scam thought she could earn $18k in a week

Three arrested over suspected involvement in ‘buy now, pay later’ job scam

The police said: “Always verify the authenticity of job offers through official channels or sources, and do not accept dubious job offers that offer lucrative returns for minimal effort.

“Do not engage or believe claims made in any messaging app group chats that you are randomly added or invited into, and do not click on suspicious URL links or download apps from unknown sources.”

Anyone who gets such messages can lodge a report using tools available on the WhatsApp and Telegram applications.

Singaporeans with details on scams or have doubts about the veracity of messages can call the police hotline on 1800-255-0000 or go to http://www.police.gov.sg/iwitness.

If in need of urgent police assistance, they can call 999.

More information can be found on http://www.scamalert.sg. Individuals can also call the Anti-Scam telephone hotline on 1800-772-6688.

MORE ON THIS TOPIC

Can you spot a scam? Find out how well you know 6 common scams in S’pore

About $750,000 lost by at least 46 victims to job scams since March.

=============

.

Over 500 scam victims filed claims in bid to recover losses from banks

The scams were not new yet the victims still fell for them because many failed to take note of the regular and widely publicised police advisories. ST PHOTO: GIN TAY

Tan Ooi Boon

Invest Editor

PUBLISHED 7 JAN 2024, 5:00 AM SGT in Straits Times.

The scams that continually plague people in Singapore have resulted in a whopping increase in claims filed against banks as some victims seek to recover their losses.

The Financial Industry Disputes Resolution Centre (Fidrec) received 509 fraud-related claims that were mostly filed against banks from July 2022 to June 2023 alone – a 95 per cent jump from the 261 cases heard in the same period in its previous financial year.

=============

.

Scams are like cockroaches, they keep evolving; let’s do more to ensure digital safety: Tin Pei Ling.

A motion on building a safe digital society will be debated in Parliament on Jan 9. ST PHOTO: GIN TAY

Zhaki Abdullah and Jean Iau

UPDATED 7 HOURS AGO on 9th Jan 2024 in Straits Times.

SINGAPORE – After an elderly resident in MacPherson fell prey to an investment scheme supposedly endorsed by then Senior Minister Tharman Shanmugaratnam, he nearly lost several thousand dollars in fraudulent credit card charges.

But after approaching his MP Tin Pei Ling for help, the man managed to get the charges waived with his bank’s help.

The man had only a “few hundred dollars” in his savings account, almost half of which he had invested in the fake investment plan, the MacPherson MP said.

Following this and other reports of residents continuing to fall for scams despite attempts to raise awareness about common scam tactics, Ms Tin told The Straits Times more needs to be done.

Ms Tin – who chairs the Government Parliamentary Committee (GPC) for Communications and Information – has, together with four other MPs, filed a motion on building a safe digital society. It will be debated in Parliament on Jan 9.

“We may not be able to totally stamp out such risk or threats because they’re like cockroaches; they somehow just keep evolving. But if we can do more, and everyone (is) willing to take on a larger share of the responsibility, we probably can protect more people, and reduce the harms or the damage to the ordinary citizen,” said Ms Tin in a phone interview with ST on Jan 8.

The other MPs who filed the motion are Ms Jessica Tan (East Coast GRC), Mr Sharael Taha (Pasir Ris-Punggol GRC) and Mr Alex Yam and Ms Hany Soh (Marsiling-Yew Tee GRC). They are also part of the GPC.

Ms Tin noted that while Singapore continues its journey to digitalise, she and her fellow MPs have observed challenges, including scams, that undermine the public’s confidence and trust towards digital transactions.

Aside from the resident who fell victim to the fake endorsement using Mr Tharman’s name, Ms Tin recounted how she was notified about a man pretending to be her brother on Telegram to get people to invest in a fraudulent scheme. She filed a police report, and the account and group were shut down.

In recent years, the authorities have introduced several measures to counter such scams. On Jan 5, it was announced that mobile phone users can approach their telcos to block all international calls, the first of a number of anti-scam measures to come in 2024.

Ms Tin said the MPs have made 13 calls to action, which she will reveal during the debate.

Shedding some light on what this entails, she said: “We are trying to push the Government to do more… to lead in some of the areas, in terms of getting corporations and private entities to share more information, for example, to be more transparent with their products and offerings, so that we can be more prepared for some of the risks of scams (or) malware.”

Ms Tin added that these corporations should also pull their weight and take on a more equitable share of the responsibility in terms of detection, deterrence and protection.

Finally, she urged members of the public to work together to promote greater awareness, and educate and empower vulnerable segments of the population, so that they will not be disadvantaged as Singapore progresses digitally.

“It’s also about what kind of desired environment we want to see in the digital world,” said Ms Tin, noting that in the real world, Singapore is relatively safe.

She added: “We talk about being inclusive, we say we should be kind and respectful to one another, (but) can we also do the same online?”

MORE ON THIS TOPIC

Can you spot a scam? Find out how well you know 6 common scams in S’pore

PM Lee warns against responding to deepfake videos of him promoting investment scams

================

.

Over $200m recovered by Anti-Scam Centre; new command targets scammers before victims make report

The ASC has frozen more than 27,300 bank accounts and recovered more than $200 million since its inception in June 2019.ST PHOTO: ALPHONSUS CHERN

SINGAPORE – More than $200 million has been recovered by the Anti-Scam Centre (ASC), with the police now targeting scammers even before people realise they have fallen prey and make a report.

At the Police Workplan Seminar on Tuesday (April 26), it was revealed that as of last month, the ASC has frozen more than 27,300 bank accounts and recovered more than $200 million since its inception in June 2019.

But while fund recovery remains a key function, anti-scam operations will now focus on upstream interventions, dismantling scam operations before victims even realise they have fallen for a scam.

Each of the seven police land divisions across Singapore now has its own Scam Strike Team comprising hand-picked officers who are experienced and specialise in fighting scams. This was revealed at Tuesday’s seminar.

The teams are dedicated units that target money mules and runners here, working closely with their colleagues and overseas counterparts to tackle and solve syndicated and transnational scam cases.

The Anti-Scam Centre was set up as a specialised unit under the Commercial Affairs Department (CAD) in 2019.

Last year, the Anti-Scam Division was formed, reorganising and consolidating all scam-fighting units under the CAD.

The division was expanded last month to become the Anti-Scam Command, which brings together all scam-fighting units across the entire Singapore Police Force.

The new command sees coordinated anti-scam operations boosted by technology that can detect and automatically alert potential scam victims even before they become prey to scammers.

When victims make a police report, it will be scanned for online monikers, websites and advertisements linked to scam activities.

These will then be taken down with the help of online marketplace platforms and telecommunication companies.

In his speech at the Police Workplan Seminar, Minister for Home Affairs and Law K. Shanmugam said scams remain a key concern, with cases rising 52 per cent over the past year.

“The police force is reorganising its resources to tackle new crime trends,” he said.

“The Anti-Scam Command consolidates investigation of all types of scams into one unit, and oversees the newly formed Scam Strike Teams in the land divisions. That will help in better sense-making, more effective crime prevention, and a faster response against scams.”

Speaking to the media, the director of CAD, Mr David Chew, said the new command partners with over 60 institutions, including local and foreign banks, non-bank financial institutions, cryptocurrency houses and remittance service providers.

Mr Chew introduced representatives from four such partners during a media session on the seminar.

They were from Standard Chartered Bank, Singtel, cryptocurrency platform Coinhako and gaming firm Razer.

Mr Chew said building close working relationships with such institutions was critical for the Anti-Scam Command to swiftly freeze accounts, recover funds and reduce losses suffered by victims.

He said the command will continue to work with banks and fintech companies to develop systems that use artificial intelligence to identify and block suspicious transactions.

Currently, only DBS Bank has a staff member co-located at the Anti-Scam Centre in the Police Cantonment Complex.

It was previously reported that both OCBC and UOB banks have plans to soon also have staff members working from the centre.

Mr Yap Jee Hoe, head of client diligence and fraud risk management at Standard Chartered Bank, said it is committed to fighting scams and it too will send a staff member to the centre.

“We remain strongly committed to protecting our customers, and to do so we have to be part of this anti-scam ecosystem,” he said.

“I do hear a lot of stories from scam victims, and it’s quite painful. I feel for them.”

He added that the partnership with the new command has proven fruitful.

Mr Yap said that just last month, the partnership enabled them to help a bank customer recover close to $300,000 which was almost lost to scammers.

“The victim was of course, very grateful,” he said.

“We hope other players will come on board to also partner the Anti-Scam Command and to further raise awareness of scams so that everyone is protected.”

.

==============

.

Can one activate it when the bank account has been taken over by the scam criminals, who have replaced the phone number, the email address, etc, to those of their own?

.

==========

.

Forum: Effective bank account kill switch must not be difficult or tedious to activate

PUBLISHED 6 HOURS AGO on 24th Feb 2022 in ST Forum.

We thank Mr Lam Jer Wei for his letter (Current phone activation process for OCBC ‘kill switch’ requires too little information, Feb 21).

We would like to clarify the intent and the process of activating the kill switch by calling the bank.

The kill switch is for use only in an emergency, such as a fraud or scam.

An effective kill switch must not be difficult or tedious to activate, and must halt an operation as quickly as possible.

In an emergency, when a customer’s bank account has been compromised, time is of the essence to quickly block the account from fraudulent transactions.

Customers are very anxious at that moment. The information needed to activate the kill switch upon calling the bank’s official contact number would therefore need to be easy to retrieve or remember.

Adding verification layers by having staff ask questions about the customer’s name, date of birth and banking relationships would slow the process tremendously.

Personal bank account log-in information such as passwords, PINs or credit card CVV security numbers are never asked for over the phone.

Once the emergency kill switch is activated, a follow-up call will be made soon after by a bank customer service executive to ensure that it was activated by the actual bank account holder and was not an act of mischief.

The customer service executive will help the account holder to remove any compromised bank account access or cards, issue new ones, deactivate the kill switch and restore accounts.

If a customer prefers to speak to a bank staff member about a compromised bank account, there is an option to do so after calling the bank’s official contact number.

This option would take longer as the staff member will first have to validate the customer though the usual authentication process.

There are other ways to activate the kill switch – via OCBC Bank ATMs or by visiting any OCBC branch.

Dennis Lee

Head of Risk and Prevention

Consumer Financial Services Singapore

OCBC Bank

.

=============

.

=

.

Hope the SPF’s anti-scam centre will set up an email address for the public to give immediate feedback to alert/inform the police of an ongoing crime in progress by criminals using phishing [fishing] scam methods.

Speed and time are the essence.

===——-

Internet scams…phishing [fishing] scams.

Banks should also set up an Internet email address for victims to reach them fast.

Phone lines will be jammed.

.

=================

.

Nearly $1 billion lost by scam victims in Singapore since 2016

Cheow Sue-Ann runs through the latest scourge: job scams

Wong Shiying

UPDATED 9 MINS AGO on 29th Jan 2022 in Straits Times.

SINGAPORE – The recent phishing saga involving customers of OCBC Bank has highlighted the epidemic of scams in Singapore, where victims have lost more than $965 million in just over 5½ years, checks by The Straits Times showed.

Scammers pocketed a record high $268.4 million in total in 2020, a figure Home Affairs and Law Minister K. Shanmugam revealed last year in a written response to a parliamentary question on scams.

It was nearly triple the $89.7 million stolen in 2016.

The authorities have acknowledged the difficulties in tackling the problem – many of the perpetrators are based overseas, and when the monies have been transferred, recovery has been hard.

But the police have had some success.

Their Anti-Scam Centre said that of the 7,400 scam reports it received in the first half of last year involving losses of more than $201.7 million, the authorities were able to recover $66 million.

Internet love scams have remained one of the most lucrative scams in Singapore since 2011.

The amount duped from victims has grown from $2.3 million in 2011 to $8.8 million in 2014 and $33.1 million in 2020.

Police said 90 per cent of the scams in Singapore had originated from overseas.

They added that they have worked closely with foreign law enforcement agencies to monitor and share information on emerging scams and conduct joint operations to cripple syndicates.

The police said that last year, the Anti-Scam Division (ASD) of the Commercial Affairs Department worked with the Royal Malaysia Police, Hong Kong Police Force and the police force in Taiwan.

MORE ON THIS TOPIC

Internet love scams in Singapore cost victims $33.1 million in 2020

Woman lost $17k she had saved for her wedding to a job scam.

“Sixteen transnational syndicates perpetrating job scams, Internet love scams and impersonation scams were busted,” the police said.

ASD oversees the Anti-Scam Centre.

Speaking to the media on Thursday (Jan 27), Deputy Assistant Commissioner (DAC) of Police Aileen Yap said the joint operations led to the arrest of 230 suspected syndicate members. DAC Yap is the assistant director of the Commercial Affairs Department’s ASD.

SPH Brightcove Video

In Singapore, police also arrested and investigated more than 7,000 scammers and money mules last year.

Some are believed to have rented out their bank accounts to scammers or assisted them by carrying out bank transfers and withdrawals.

The Covid-19 pandemic has not slowed down the syndicates, with more victims falling for job scams, the Anti-Scam Centre said.

Some victims refuse to believe they have been scammed, think cops are the bad guys.

In the first six months of last year, there were 658 cases of job scams – a 16-fold increase from just 40 in the same period in 2020.

“Scammers are quick to adapt their tactics and scripts to keep up with the current climate.

“During the pandemic, scammers have impersonated government officials to phish for personal particulars from victims,” police said.

Criminologist Olivia Choy, from Nanyang Technological University’s psychology department, said financial and emotional stress triggered by the pandemic could have made people more vulnerable to scams.

“Such stressors can lead to poorer decision-making, and with more people going online for work and leisure, there is an influx of potential victims for opportunistic scammers,” she added.

Additional reporting by David Sun

Correction note: This article has been edited for clarity.

MORE ON THIS TOPIC

Scam scourge: How can we fight it?

Stop scams: Counting the cost of love, sex and money scams.

Six anti-scam principles to follow

The Home Team Behavioural Sciences Centre developed a 6S Anti-Scam Self-Protection Principles to help Singaporeans defend themselves against scams. They are:

Spot the signs – Recognise the tactics that scammers use.

Stop and think – Ask yourself or others if a statement, message or job offer could be true.

Slow down, don’t rush – Do not rush into providing your personal or banking details.

Speak to others – Check with others to verify the authenticity of a claim before doing anything.

Safeguard personal details and passwords – Never disclose personal information, even if the request appears to be legitimate.

Seek help – Talk to friends or family members for advice or support if you have been impacted by a scam.

MORE ON THIS TOPIC

4 common types of scams and how to recognise them

Is contactless payment safe? 5 tips to protect yourself in the wake of OCBC SMS scams.

Helplines

Anti-Scam Hotline: 1800-722-6688 (9am – 5pm)

National Care Hotline: 1800-202-6868 (8am – 12am)

Mental well-being

Institute of Mental Health’s Mental Health Helpline: 6389-2222 (24 hours)

Samaritans of Singapore: 1800-221-4444 (24 hours) /1-767 (24 hours)

Singapore Association for Mental Health: 1800-283-7019

Silver Ribbon Singapore: 6386-1928

Tinkle Friend: 1800-274-4788

Community Health Assessment Team 6493-6500/1

Counselling

TOUCHline (Counselling): 1800-377-2252

TOUCH Care Line (for seniors, caregivers): 6804-6555

Scam alert: From OCBC SMS scam to fake Iras e-mails, here’s what you need to know

Interactive: How a love scammer’s 3-month ruse to swindle $165k got exposed.

.

======

Be fast….speed and unobstructed feedback is very important..

=======

Forum: Police will review spam reporting under I-Witness

PUBLISHED FEB 24, 2022, 2:00 AM SGT in ST Forum.

Mr Cheong Tuck Kuan suggested making it easier for members of the public to report spam messages, such as through a single number (Make it easier to report spam SMSes, Feb 18).

As unsolicited spam messages may be sent by a range of entities, and for different purposes, there are different platforms for members of the public to report them so that the appropriate follow-up actions may be taken.

For spam marketing messages that are not crime-related, members of the public should directly contact the company concerned to ask to be removed from their marketing list.

Those who do not wish to receive telemarketing messages can also register their Singapore telephone numbers with the Personal Data Protection Commission’s Do Not Call Registry, and turn on the anti-spam features on their mobile devices.

Suspected scam calls and messages can be reported via the in-app reporting function of ScamShield, a mobile app which filters out scam messages and blocks unsolicited calls from scam-tainted phone numbers.

The information will then be forwarded by the National Crime Prevention Council to the Anti-Scam Centre for follow-up actions.

Information on spam messages related to criminal activity such as scams or unlicensed moneylending messages can also be shared via the I-Witness online portal (http://www.police.gov.sg/iwitness).

We will review how we can simplify the reporting under I-Witness.

Brenda Ong (Superintendent)

Assistant Director, Public Communications Division

Public Affairs Department

Singapore Police Force

=

Your credit card number is everywhere when you use it to make a purchase…

Best is not to use it if one is paranoid.

=======

.

Forum: Not safe to let credit cards out of sight at restaurants

PUBLISHED 5 HOURS AGO on 25th Feb 2022 in ST Forum.

I refer to the article, “Time to ban asking for credit card details over the phone” (Feb 1), which describes the card verification value (CVV) as “to a credit or debit card what a security gate is to protected premises”.

I would like to highlight another practice that could also compromise the CVV – handing your credit card to the waiter for bill payment at a restaurant. Isn’t there a risk of the credit card details being copied?

Can restaurants be made to implement a system where the payment device is brought to the dining table? This is widely practised in Europe. If that cannot be done, then let us queue at the counter for payment. It is much safer than letting our credit cards out of sight.

Jacqueline Lim

.======

What else is missing….Solutions?

Do we know that once you give your OTP, etc, to the criminals, your account is completely in their hands, under their control, and that you will not be able to give further instruction to deactivate your account or take back control of your account?

Do we know that once your account is out of your control, your phone number will be changed, and any warning messages will go to the criminals’ phone number, not yours any more?

You are completely cut off, and will be in the dark at the mercy of the criminals to cream off your money immediately?

.

=======

.

Forum: Current phone activation process for OCBC ‘kill switch’ requires too little information

PUBLISHED 4 HOURS AGO on 21st Feb 2022 in ST Forum.

To protect its customers, OCBC Bank recently implemented a “kill switch” which allows customers to freeze their accounts over the phone or at an ATM (OCBC customers can freeze accounts with ‘kill switch’, Feb 17).

While I commend the bank’s intentions, the process by which the kill switch can be activated over the phone seems flawed.

It currently requires either a 16-digit credit/debit card number or 10-digit ATM card number, and the customer’s NRIC number.

These are pieces of information that are collected by organisations such as telcos and insurance companies for bill payment purposes.

Given the number of data breaches that have occurred, it would be naive to think that this information is not readily available on the Dark Web.

Furthermore, unlike a password, a customer’s credit card number usually is not changed and his NRIC number remains constant.

The implication is that bad actors can essentially cause a nuisance by locking out account holders.

The freezing of accounts should be done only after securely authenticating a customer’s identity. If not, I hope OCBC will let customers opt out of phone activation of the kill switch.

Lam Jer Wei.

.

======

.

I refer to “OCBC introduces ‘kill switch’ to allow customers who have been scammed to freeze their own accounts’ [Today, 16th Feb 2022].

Criminals of scams will try to open their own bank account/s with fake or stolen passport or i/c to avoid detection, and will use the account for one-hit only, and after that, they will disappear into the crowd untraceable.

Bank officers are not well-versed to detect a fake passport easily.

I would like to suggest the following extra protective measures:

a] use of passport to open a bank account must be supported by a work pass issued by the Govt. The Govt shall provide an App site for the banks to submit the details of the passport and work pass within two working days to detect fraud, if any;

b] use of i/c card to open the bank account, the banks must submit the details of the i/c within two working days to a Govt’s App site to detect i/c fraud or stolen i/c.

I hope these additional measures will help banks and the SPF to fight against scams.

.

=======

.

Fake bank accounts by criminals for one-hit only and disappear into the crowd.

They use stolen/fake passport or i/c to open bank account.

Solutions to stop this? How?

.

=========

.

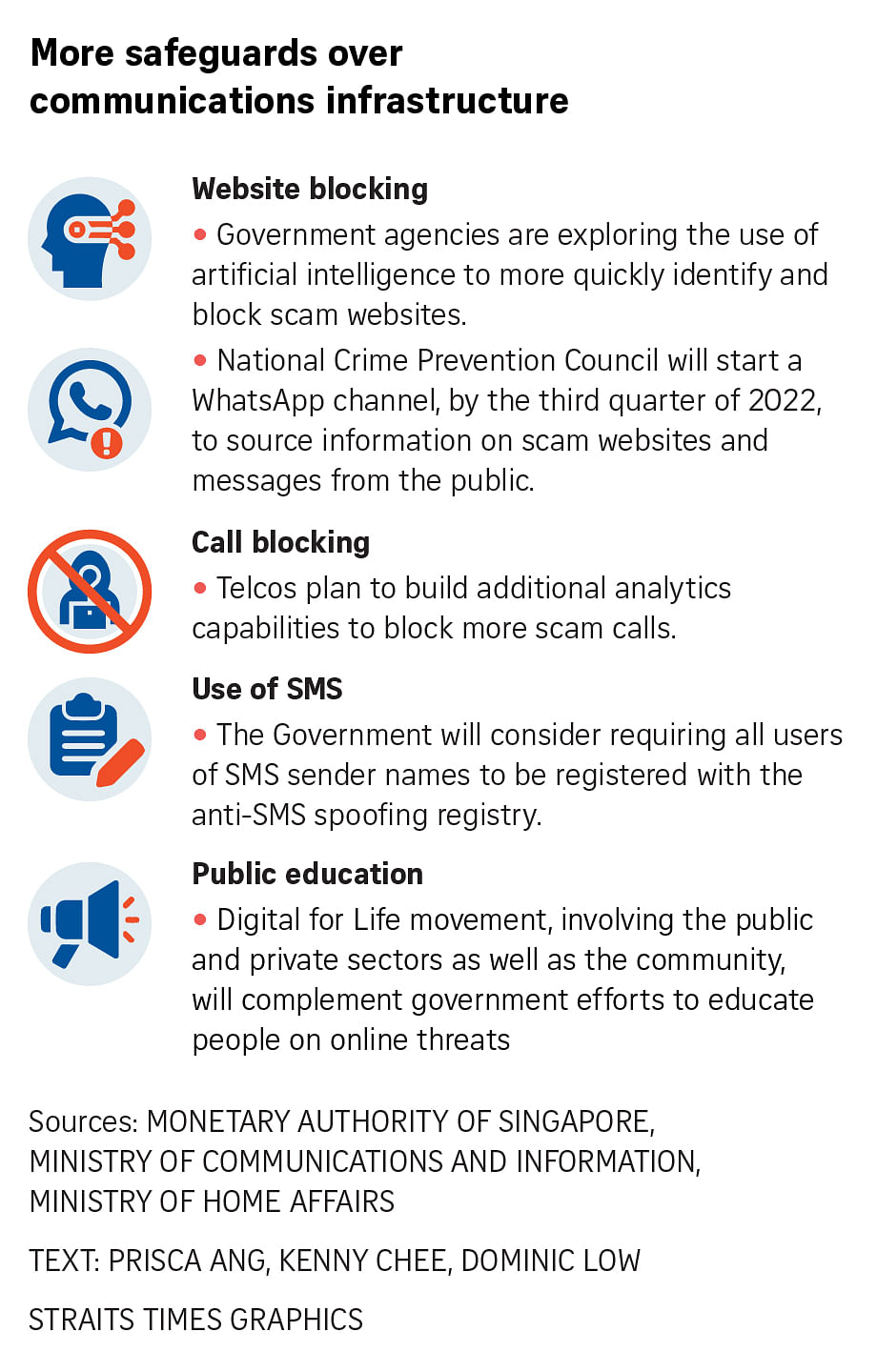

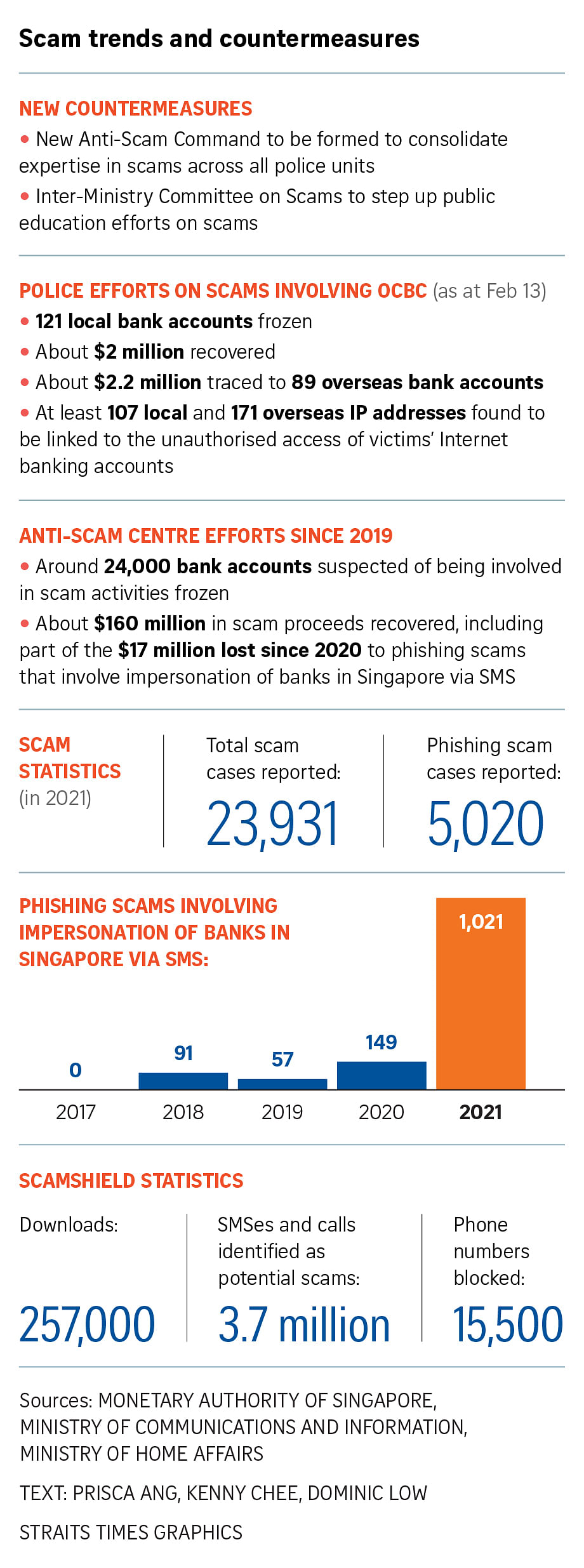

$2m from OCBC scams recovered, 121 local bank accounts frozen: Desmond Tan

Overall, there were 23,931 cases of scams reported last year, of which 5,020 were phishing scam cases.PHOTO: ST FILE

SINGAPORE – The police have frozen 121 local bank accounts and recovered about $2 million lost by victims in phishing scams targeting OCBC Bank customers as at Sunday (Feb 13), said Minister of State for Home Affairs Desmond Tan.

Providing an update on the ongoing investigations into the OCBC phishing scams which took place last December, Mr Tan also said that about $2.2 million of victims’ funds have been traced to 89 overseas bank accounts.

“Many of the scam websites used in the phishing scams were hosted by web hosting companies based overseas,” said Mr Tan, who chairs the Inter-Ministry Committee on Scams (IMCS) set up in April 2020.

Specifically, at least 107 local and 171 overseas Internet protocol (IP) addresses were linked to the unauthorised access of the victims’ internet banking accounts.

He was replying MPs Tan Wu Meng (Jurong GRC), Sitoh Yih Pin (Potong Pasir SMC) and Dennis Tan (Hougang SMC), who asked for an update in Parliament on the ongoing investigations into the OCBC phishing scams.

The police have commenced investigations into the local IP addresses linked to the scams and the owners of the local money mule accounts.

The police are also working with Interpol and foreign law enforcement agencies to investigate the beneficiaries of the funds transferred overseas and the hosts of the scam websites.

Mr Tan was not able to divulge more information as investigations were still ongoing.

But he noted that OCBC customers fell prey amid a sharp increase in the number of scams reported in Singapore.

Phishing scams involving SMSes that impersonated banks in Singapore have increased significantly, from 149 cases in 2020 to 1,021 last year. The OCBC scams were the largest case involving such fraudulent schemes.

Overall, there were 23,931 cases of scams reported last year, of which 5,020 were phishing scam cases.

MPs Ang Wei Neng (West Coast GRC) and Cheng Li Hui (Tampines GRC) asked for the number of similar scams reported over the past five years and if the police were well-resourced to tackle scam-related crime.

Mr Tan said: “The use of a combination of highly orchestrated tactics, involving spoofed SMSes appearing in the same thread as genuine messages from the bank and links directing victims to a scam website, as well as the large number of customers targeted in the OCBC scams, show that the threat is now significantly heightened.”

He also said that people aged between 20 and 39 formed the largest group of victims of phishing scams and those related to jobs, e-commerce, investments, loans, China official impersonation and fake gambling platforms.

The largest group of victims of social media impersonation scams and those involving Internet love and fake friend calls were those aged between 40 and 59.

Responding to a question by Associate Professor Jamus Lim (Sengkang GRC) about unauthorised transactions made on credit cards in the past year, Mr Tan said card fraud cases reported by major credit card issuers here to the Monetary Authority of Singapore made up less than 0.1 per cent of total credit card transactions.

Mr Tan noted that the police are extremely stretched, with officers trying to cope with increasing workload and expectations without a proportionate increase in manpower.

But the Anti-Scam Centre has frozen around 24,000 bank accounts suspected of being involved in scam activities and recovered about $160 million in scam proceeds since it was set up by the police in 2019.

The amount recovered included part of $17 million lost since 2020 to about 1,300 cases of phishing scams involving spoofed SMSes that impersonated banks here, added Mr Tan.

He emphasised that recovery of money lost to scams is difficult, adding that where such sums have been recovered by the police, it involved the help of financial institutions.

Mr Tan noted that the police will be forming an Anti-Scam Command this year to consolidate expertise in scams across all police units, thereby improving coordination of anti-scam enforcement and investigations.

The police uses technology to automate manual work processes in its fight against scams, including the generation of electronic production orders to banks for the freezing of bank accounts associated with scams.

“This allows police resources to focus on critical investigations and enforcement work,” Mr Tan said.

The police is also using other technology, such as the ScamShield app, to crowdsource information on scam calls and SMSes.

Mr Tan said ScamShield – developed by the National Crime Prevention Council in collaboration with Open Government Products, a division of the Government Technology Agency, and the police – has been downloaded about 257,000 times to date.

About 3.7million SMSes and calls have been identified as potential scams by the in-app algorithm and by user reports through the app, while about 15,500 phone numbers have been blocked.

“ScamShield picked up and filtered about 2,000 scam messages used in the OCBC phishing scams,” said Mr Tan. “Unfortunately, a lot more scam messages managed to reach the SMS inboxes of ScamShield users, mainly because they appeared in the same thread as legitimate messages.”

He said this gap will be plugged to counter spoofed SMSes.

While ScamShield is currently only available for iOS devices, Mr Tan said an Android version is planned to be released in the next few months.

The IMCS will step up public education efforts on scams. For example, it has started working with the Agency for Integrated Care, the Ministry of Education, the Ministry of Manpower and MoneySense to educate seniors, students, migrant workers and professionals on scams.

Using stolen or fake passport or i/c card to open bank account by criminals for a one-strike hit and then disappear into the crowd. Solution to stop this ruse? How?=

.

============

.

Police freeze 121 local bank accounts linked to OCBC scam; about S$2 million recovered

15 Feb 2022 03:17PM(Updated: 15 Feb 2022 10:41PM) in channelnewsasia.com

SINGAPORE: Singapore police have frozen 121 local bank accounts as of Feb 13 (Sunday) amid ongoing investigations into a recent SMS phishing scam targeting OCBC bank customers, while recovering about S$2 million of victims’ money.

In addition, about S$2.2 million has been traced to 89 overseas bank accounts, said Minister of State for Home Affairs Desmond Tan on Tuesday.

=======

.

‘I’ve been scammed’: PM Lee on how he himself was victim of an online scam

PM Lee Hsien Loong said he was the victim of a fake website, where an item he ordered never arrived.PHOTO: ST FILE

About $660 million is lost in scams annually, with Singaporeans losing nearly $2 million a day to such crimes, he said during an interview with the Chinese media at the Istana on April 28.

“It is earth-shaking to be robbed of that amount daily, but it is happening on the internet every day,” PM Lee said. “This is the hard-earned money of the people and could even be an elderly person’s life savings meant for his last 20 to 30 years. His money is wiped out overnight.”

“We’ve done what we can, but it is still heartbreaking, and we are still thinking what more can be done to help the victims,” he added. “Maybe it is also about how we can prevent ourselves from being scammed.”

PM Lee shared that he himself had been the victim of a fake website, where an item he ordered never arrived.

“I’ve been scammed,” he said. “I thought it was real, but it didn’t come for a long time.”

“The online world is a colourful one, but it is also a big headache,” he added.

More than 90 per cent of Singaporeans have internet access. While it is important to have online connectivity to maintain a normal relationship with people, fake news and deepfakes have made it difficult to decipher truth from falsehood, he said.

Children should be taught to ask questions when they see a piece of news, such as whether it is credible, who sent it, what is the motive of the sender and if there is a need to verify the truth with reliable news sources, he added.

“If you see a piece of news stating that Lee Hsien Loong is selling Bitcoin, you better go check, because it is bogus unless there is something wrong with me.”

PM Lee’s identity has been used by scammers in various schemes. Some people have alerted him to such scams by sending him screenshots and expressing their anger.

“It has happened so often to me that I don’t react to such scams any more,” he said. “I told them: ‘Don’t be angry, calm down, this is a recurring issue, and we will take action.’”

While he occasionally takes to his Facebook page to remind everyone to be careful of scammers, he cannot keep up with the fake news.

“My Facebook cannot be like your bank app, dispatching security advisories to everyone daily.”

Falling victim to scams does not mean one is stupid, and even intelligent people can be scammed, he said.

“Sometimes, the bank staff may step in to help you from losing your life savings to scams. You may be scolding them, asking: ‘Why are you stopping me? I know what I’m doing, do you think I have Alzheimer’s disease?’” said PM Lee.

“You may not have Alzheimer’s, but you have fallen for a scam unknowingly. This is a very serious problem.”

The media also needs to guard itself from reporting fake news unwittingly, he said.

“It is very likely to happen, because even with your vigilance, it may slip through the cracks one day.”

The scammers are always coming up with new and better tricks, he said.

“This is an ever-evolving problem, and we don’t have a strategy to deal with it every time. It is something we have to keep tackling, and other countries are facing the same challenge.”

The problem is widespread elsewhere, including in China and probably in the neighbouring countries too. Their numbers may seem lower because many scams go unreported, PM Lee added.

“In Singapore, scams are reported to the police, so there is hope that we can manage this problem.”

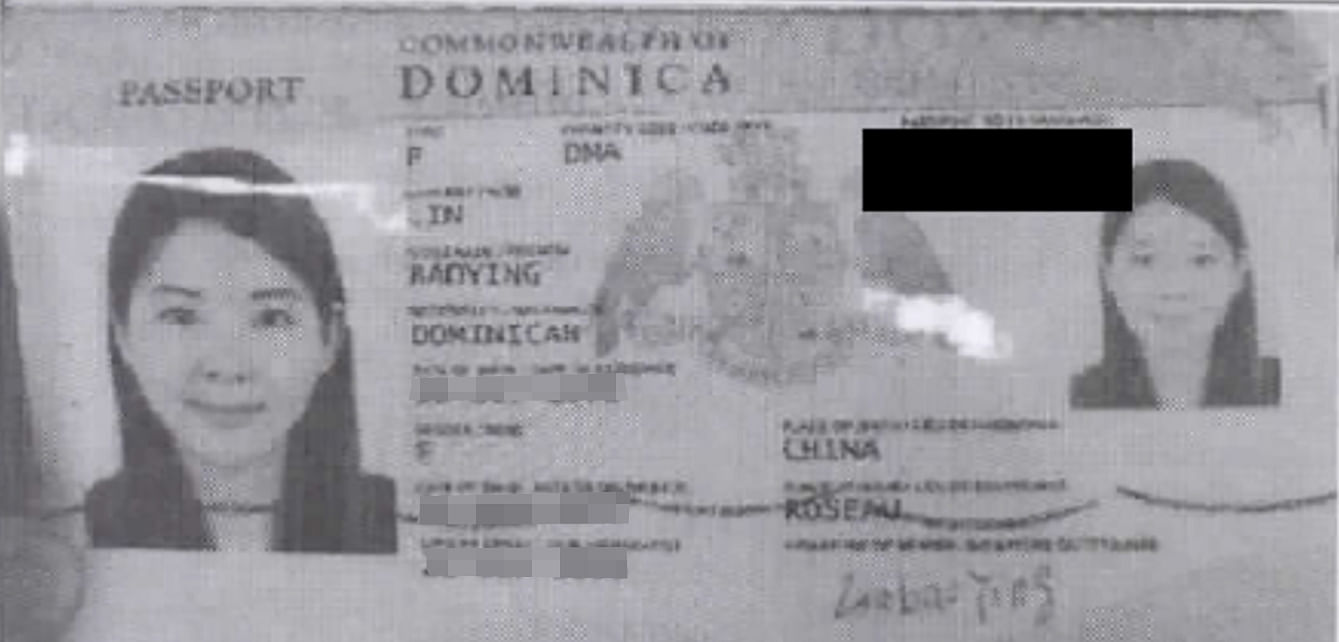

On May 21, she was handed one new charge of forgery, two charges of using forged documents and four charges of possessing benefits of criminal conduct.

According to court documents, Lin allegedly engaged in a conspiracy with one Liu Kai and one Li Hongmin to commit forgery to cheat Bank Julius Baer & Co on or before Nov 24, 2020.

Separately, Lin allegedly submitted a forged document – purportedly an agreement for the sale of a property in Macau – to UOB Kay Hian, to justify a deposit of HK$7.5 million (S$1.2 million) into her account.

She also allegedly submitted a forged document, which she claimed was a loan agreement, to OCBC Bank to justify a deposit of HK$5 million into her account.

Aside from her seven new charges, the two forgery charges handed to her in August 2023 were amended to using a forged document as a genuine one. PHOTO: COURT DOCUMENTS

The other four new charges stated that Lin allegedly possessed HK$209 million, which represented benefits of criminal conduct.

She has had over $215 million in assets seized or frozen by the authorities.

This money laundering case has seen the seizure of assets, including luxury homes, cars, watches and bags, worth over $3 billion.

It was revealed in earlier court proceedings that Lin and one of those arrested in the raid, Zhang Ruijin, 45, were lovers and that they have known each other for more than a decade.

They were arrested in a bungalow on Pearl Island in Sentosa Cove.

Before her arrest, Lin lived on Sentosa with Zhang while her 15-year-old daughter lived with a maid in Beach Road.

Lin calls Zhang her husband, though they are not officially married.

On April 30, he was sentenced to 15 months’ jail, the highest jail term meted out in the case so far. He pleaded guilty to one money laundering charge and two forgery charges.

Five others have been convicted.

Su Wenqiang, Wang Baosen, Vang Shuiming, Su Haijin and Su Baolin were each jailed between 13 and 14 months.

The six men who were dealt with have each agreed to forfeit between $5.9 million and $180 million in assets to the state.

So far, over $541.9 million in assets has been forfeited by them.

Responding to questions from Members of Parliament, he noted that the police have found at least 107 local and 171 overseas IP addresses linked to the unauthorised access of victims’ Internet banking accounts.

Many of the scam websites used in the phishing scam were hosted by companies based overseas, he added.

Police are investigating the local IP addresses linked to the scam and the owners of the local money mule accounts.

They are also working with Interpol and foreign law enforcement agencies to investigate the beneficiaries of the funds transferred overseas, as well as the hosts of these scam websites, said Mr Tan.

The SMS phishing scam involving OCBC came amid a rise in the number of scams reported in Singapore.

Last year, 23,931 scam cases were reported, including 5,020 phishing scams.

These figures mark a four-fold increase from 2017 – when there were 5,147 cases of scams reported, with 16 being phishing scams, said Mr Tan, who also chairs the Inter-Ministry Committee on Scams.

Specifically on phishing scams involving SMSes impersonating banks, there were no such cases reported in 2017.

They started emerging in 2018 with 91 cases, followed by 57 cases in 2019 and 149 cases in 2020. This surged further to 1,021 last year.

Responding to another parliamentary question, Mr Tan noted that card fraud cases reported by major credit card issuers in Singapore formed less than 0.1 per cent of total credit card transactions last year.

The Monetary Authority of Singapore (MAS) and the Singapore Police Force (SPF) do not track the percentage of funds recovered for these unauthorised credit card transactions, he added.

NEW ANTI-SCAM COMMAND AND USING TECH

To better combat scams, the police will form an Anti-Scam Command this year to consolidate expertise in scams across all SPF land units, thereby improving its coordination of anti-scam enforcement and investigations.

The new command, said Mr Tan, will also oversee the newly formed Scam Strike Teams in the seven police land divisions.

Last year, the ASC conducted 26 islandwide anti-scam operations and arrested about 7,500 money mules and scammers.

The unit has also frozen about 24,000 bank accounts suspected of being involved in scam activities since 2019, while recovering nearly S$160 million in scam proceeds.

Mr Tan pointed out that the recovery of money lost to scams is “very difficult”.

“Where we have been able to, it involved close partnerships with financial institutions, particularly by having a DBS staff co-located with SPF at the ASC to provide swifter and real-time coordination and intervention.”

As such, the ASC and MAS are working with more banks to co-locate their staff at the ASC so as to enhance the centre’s capabilities to freeze accounts and trace the flow of funds, he told the House.

The ASC also taps on technology, for instance, in automating manual work processes so that police resources can be focused on critical investigations and enforcement work.

RAMPING UP PUBLIC EDUCATION

But enforcement by itself is not sufficient, said Mr Tan, adding that the “best defence” against scammers is “a discerning public”.

The Government has been working on this, such as by rolling out an anti-scam public education campaign “Spot the Signs. Stop the Crimes”.

“As part of this campaign, we have disseminated materials advising the public on scam prevention tips, such as never to share one-time-passwords or your OTPs, with unverified parties and to be aware of requests for gift cards or online credits,” he said.

Authorities have also rolled out prevention initiatives targeted at specific segments of the population.

While scam victims are of a wide range of ages, Mr Tan noted that different profiles of victim fall prey to different types of scams.

For instance, young adults between 20 and 39 years old have formed the largest group of victims when it comes to phishing scams, job scams, e-commerce scams, investment scams, loan scams, China official impersonation scams and fake gambling platform scams.

For social media impersonation scams, Internet love scams and fake-friend call scams, adults between 40 and 59 years old were the most vulnerable.

In his speech, Mr Tan also urged more people to download the ScamShield app developed by the National Crime Prevention Council and the Government Technology Agency.

The app identifies and filters out scam messages using artificial intelligence, sending them to the phone’s junk folder. It also blocks scam calls from phone numbers used in other scam cases or reported by ScamShield users.

Since its launch in November 2020, the app, which is currently only available for iOS devices, has been downloaded about 257,000 times, Mr Tan said.

About 3.7 million SMSes and calls have been picked up as potential scams by the in-app algorithm and reports from users. Nearly 15,500 phone numbers have also been blocked.

Specifically on the OCBC scam, ScamShield picked up and filtered about 2,000 scam messages.

“Unfortunately, a lot more scam messages managed to reach the SMS inboxes of ScamShield users mainly because they appeared in the same thread as legitimate messages,” said Mr Tan.

To address this gap, Communications and Information Minister Josephine Teo said in her ministerial statement that authorities are considering requiring all users of alphanumeric IDs to be registered in a pilot SMS sender ID protection registry, among others.

Authorities are also working towards developing and releasing the Android version of ScamShield in the “next few months”, Mr Tan said.

Editor’s note: Following an update by MHA, this article has been updated to correct the number of SMSes and calls that have been picked up as potential scams by the in-app algorithm and reports from users.

Source: CNA/sk(cy)

.

=========================

.

OCBC introduces ‘kill switch’ to allow customers who have been scammed to freeze their own accounts

Aaron Low/TODAYOnce the kill switch is activated, no transactions – whether done digitally, via an ATM or at branches – can be made, said OCBC.

A kill switch feature has been rolled out by OCBC bank

It will allow bank customers to freeze their own accounts if they suspect they are victims of fraud

Once the kill switch is activated, no transactions can be made, whether they are done digitally, via an ATM or at bank branches

It can only be deactivated by an OCBC bank employee

SINGAPORE — Customers of OCBC bank will now be able to freeze their own accounts by activating a “kill switch” if they believe that they have fallen victim to a scam.

The bank said in a press release on Wednesday (Feb 16) that the kill switch will “immediately freeze” all of the following:

ADVERTISEMENT

Cash withdrawals and deposits, including salary credit

Incoming and outgoing funds transfers done in here or overseas

Bill payments

Incoming and outgoing general interbank recurring order (Giro) transactions

Network for electronic transfers (Nets) transactions

Visa and MasterCard transactions using automated teller machine (ATM) credit or debit cards physically and digitally

Digital banking transactions, including on the OCBC Pay Anyone mobile application

A similar feature will be made available at all OCBC ATM machines by March.

“Once the kill switch is activated, no transactions — whether done digitally, via an ATM or at branches — can be made. Even recurring or pre-arranged fund transfers will be disabled,” OCBC said.

The announcement by the bank comes in the aftermath of a recent phishing scam that hit 790 OCBC customers who lost a total of S$13.7 million to the scammers.

The Singapore-based bank completed arrangements to reimburse all the victims with “goodwill payments” late last month.

The scam prompted Finance Minister Lawrence Wong to issue a ministerial statement on Tuesday that touched on the measures banks and authorities were mulling over to tackle the problem.

ADVERTISEMENT

Among the measures that Mr Wong raised was the possibility of allowing bank customers to freeze their accounts without having to contact the banks.

HOW TO ACTIVATE THE KILL SWITCH

In its press release, OCBC outlined two ways customers can activate the kill switch in the event that they suspect they are a victim of a scam, or if they believe key account-related details have been otherwise compromised.

The first will require the customer to call OCBC’s official contact number at 1800 363 3333 or +65 6363 3333, if they are calling from overseas.

Enter their 7-digit National Registration Identity Card (NRIC) number followed by the hash key

Press 1 to confirm their NRIC number

Enter 16-digit credit or debit card number, or 10-digit ATM card number

Press 1 to confirm card number

Press 1 to confirm account and cards suspension

Press 0 at any time to speak with a customer service executive

The second method will require them to visit an OCBC ATM machine. Next, they will need to:

Login with an ATM/debit/credit card and personal identification number

Select “More Services”

Select “Suspend your accounts and cards”

Select “Confirm”

OCBC said that a customer service executive will contact the customer after the kill switch is activated to remove compromised bank account access or cards, and issue new ones.

“Only a bank branch employee or customer service executive can deactivate the switch — and would only do so after receiving duly verified instructions from the customer,” OCBC said.

Once the kill switch is deactivated, the customer’s account will return to normal and all settings before the account suspension — including Giro arrangements and future-dated funds transfers — will be reinstated.

Aside from the upcoming kill switch, OCBC said that it had already introduced on Jan 18 a dedicated fraud hotline for customers to seek assistance for incidents of suspected fraud through the bank’s official contact number.

Delaying by at least 12 hours before a new soft token can be activated on a mobile device

Lowering to S$100 or below the default threshold for sending transaction notifications to customers

In response to TODAY’s queries, United Overseas Bank (UOB) said that it is looking into rolling out a similar measure at its ATMs that will allow customers to freeze their accounts as well.

UOB did not give details on whether it will have a similar kill switch for customers, but said that customers can, at present, call a dedicated hotline to have their accounts frozen if they suspect they have fallen victim to a scam.

Other banks such DBS and Maybank similarly said that customers may call their respective 24-hour hotline to block access to their accounts.

DBS said that its debit and credit cardholders can already personally manage security access on their card accounts via the payment control features on its digital banking app.

These include:

Initiating an instant lock of their cards

Enabling or disabling online e-commerce transactions

Switching off or on the ability to make contactless and mobile wallet payments

“We are currently evaluating self-managed options that allow customers to block access to their bank accounts in the event that they may have been compromised,” DBS said.

“These options must be simple to use, and more importantly, minimise any disruptions to our customers’ scheduled payment arrangements (such as tax and Giro payments).”

Maybank said that it is exploring self-service options so that customers may react quickly in cases of suspected fraud.

.

=========

.

Police rescue suicidal victims, work with telcos and foreign counterparts to stop scams

(From left) Wise Asia-Pacific’s head of compliance for Asia-Pacific Genevieve Noakes, senior investigation officer Quek Kee Boon, Deputy Assistant Commissioner Aileen Yap and Assistant Superintendent of Police Teng Chin Hock.ST PHOTO: LIM YAOHUI

SINGAPORE – Concerned that a scam victim in her 50s was not taking his calls, senior investigation officer (SIO) Quek Kee Boon visited her home last month and noticed the distinct smell of gas coming from her apartment.

SIO Quek, who is from the police’s Anti-Scam Division (ASD), said the woman was so weak from inhaling the gas that she was lying on the floor when she opened the door.

She said she wanted to end her life because she was distraught over losing her life savings of $100,000 to scammers.

SIO Quek was relating the incident at a police media briefing on Monday (Feb 14) to explain how the police are tackling scams.

The ASD, which comes under the Commercial Affairs Department, coordinates the police’s anti-scam investigations and enforcement.

The woman was duped in a China officials impersonation scam.

SIO Quek said the woman had transferred the money while under stress as the scammers had claimed she was being investigated by the police in China over money laundering offences.

To prove her innocence, she was told she had to transfer all her savings into one of her accounts for investigation purposes. She was also instructed by the scammers to take a bank loan of $72,500.

It was a significant sum to the unemployed mother of two.

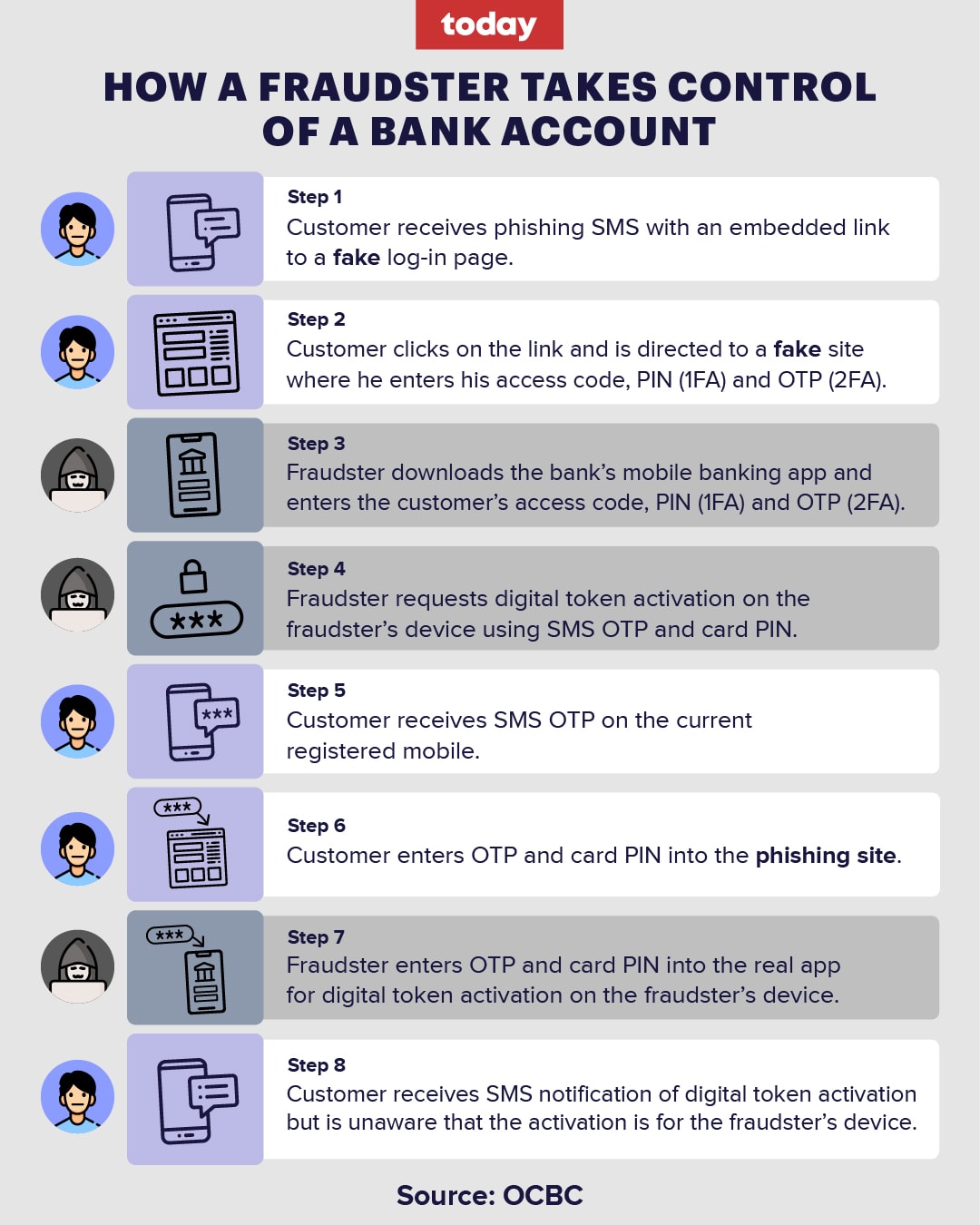

After instructing the victim to relinquish her one-time password, the scammer seized control of her bank account.

Recounting his visit to the woman’s home, SIO Quek recalled knocking persistently on her door until she finally opened it.

“She was lying on the ground, using a wooden pole to open the door. When I asked her what happened, she said she had turned on the gas (stove) to try to commit suicide,” he said.

The police contacted her family members about the incident and also offered her care support when she was discharged from hospital.

Since then, the police have recovered at least $70,000 and returned the money to her. Her condition has also stabilised.

SIO Quek said: “In extreme cases, scam victims can resort to ending their lives. I’m glad I could save her at that point in time.”

In 2021, there were 23,931 scams reported, a 52.9 per cent increase from the 15,651 cases in 2020.

Speaking to reporters on Monday, Deputy Assistant Commissioner (DAC) Aileen Yap said: “This is a life we saved but we are not sure how many we did not save.”

Between September 2021 and November 2021, the police conducted three islandwide anti-scam operations targeting money mules linked to job scams, which last year were the most reported scam type.

The operations led to the arrests of 135 individuals.

Another 141 were investigated for selling their bank accounts or relinquishing their Singpass credentials so syndicates could open bank accounts to siphon monies stolen in scams.

Last year, the police froze more than 12,600 bank accounts, recovering more than $102 million stolen in scams.

As part of enforcement efforts, the police also worked with telecommunication companies and online marketplaces to terminate more than 3,300 mobile lines and reported more than 17,300 WhatsApp lines involved in suspected scams.

The police also used technology to fight scams, launching Project Awakenings last December to identify and warn potential victims of investment scams by sending them targeted SMS advisories.

They also worked with foreign law enforcement agencies and raise awareness of scams among the public.

Police said scams last year constituted 51.8 per cent of overall crime, up from 42 per cent in 2020.

DAC Yap said the ease of online payment methods has made it more convenient for scammers to transfer money quickly.

She said: “Singapore has really become more vulnerable (to scams) with digital payments and enhanced communication channels such as Telegram and WhatsApp.

“It is extremely important for us to work together with various key stakeholders to halt the flow of money, whether it’s from a bank account, e-wallet or cryptocurrency account.

“We cannot emphasise enough that fighting scams is a community effort.”

One can activate [unlock] or deactivate [lock] the YouTrip mobile wallet debit card [card issued by Master Card] via one’s mobile phone.

I hope this feature will be made available for credit card, debit card, ATM card and manual token to be easily locked or unlocked via one’s mobile phone or computer.

.

============

.

Forum: Banking products need emergency stop feature

PUBLISHED 11 HOURS AGO on 11th Feb 2022 in ST Forum.

I have a YouTrip mobile wallet debit card which is managed by the provider’s app.

Besides being able to top up the card and check my balance, I can also pause use of the card immediately. If I lose my card or there is any unusual transaction, I can freeze the card in a matter of seconds.

In the light of the spate of phishing scams, I wonder why this has not been implemented for all vulnerable banking products, starting with bank accounts and credit cards. All major retail banks in Singapore already have established websites and apps through which this could be implemented.

Such an “emergency stop” button is common for safety purposes in places of higher risk such as at petrol stations and near heavy machinery, for example.

In the financial space, such a function lets the user temporarily pause all transactions to prevent or minimise losses in fraudulent transactions while he tries to contact the financial institutions.

Daniel Tan Yong Nam

.

.

=========

.

I have gone back to using the manual token.

I also have separate ATM cards and use only one account for making payments or drawing cash at ATM. I keep the balance in this account low, very low.

Why?

The criminals have to steal my token, my mobile phone, ATM cards, and Mac Book computer first. Can they? Unless they break into my house.

The digital token…they do not have to visit my house.

.

=======

.

Forum: Don’t assume customers need every digital banking feature

Banks should not assume that everyone wants or needs to use all of a bank’s many digital transaction features. This is especially so for features that allow for quick and easy payment or transfer of money out of the bank accounts.

In view of the recent scamming and phishing cases, banks should consider an opt-in feature in which account holders have to actively choose to opt in to a particular payment feature, instead of being accorded the feature by default.

One example is PayNow, which is fast and convenient. I tried to deactivate PayNow but it does not seem possible for account holders to do so.

Deregistering one’s mobile number from PayNow only makes it impossible for others to send money to you.

Scammers who have gained access to an account can still add a phone number, to receive money.

The convenience of digital banking transactions should be weighed against the risk involved, as no system is foolproof. Account holders should have the right to decide which features to enable.

Ng Seng Kiat.

.

==========

.

All about money.

Why some lose their money easily and others do not? Casual factors?

Greed, ego and fear, but where do all these three stem from?

.

=======

.

Forum: Police take multi-pronged approach to combat scams

PUBLISHED 5 HOURS AGO on 28th Jan 2022 in ST Forum.

We refer to Ms Yap Yong Xian’s letter, “No way to recall funds after job scam” (Jan 24).

On Nov 26, the police received a report from Ms Yap that she was scammed after responding to a job advertisement via Telegram. Upon receiving the report, the police froze the bank accounts suspected to be involved in the scam.

Investigations into Ms Yap’s case and related cases are ongoing.

Ms Yap asked about the role of the police in scam cases and the recovery of funds for victims.

The police adopt a multi-pronged approach to combat scams.

First, we have strengthened enforcement. The Anti-Scam Centre (ASC) was set up in June 2019 to disrupt scammers’ operations and mitigate victims’ losses.

Upon receipt of reports, the ASC works with local banks to freeze accounts suspected to be involved in the scams. However, it is difficult to recover money that has already been transferred to scammers, and even more so if it has been moved overseas.

Since 2019, the police have investigated more than 10,000 scammers, and bank account holders who relinquished their bank accounts to scammers or assisted scammers in conducting bank transfers.

The police also stepped up collaboration with foreign law enforcement agencies. Last year, nine transnational job scams were busted through joint operations with the Royal Malaysia Police and Hong Kong Police Force.

Second, the police partner various stakeholders to prevent scams. For example, we worked with the National Crime Prevention Council (NCPC) and GovTech to develop and launch the ScamShield app in November 2020.

Third, the police actively promote public awareness of scams. We have issued numerous advisories to warn the public against scams, and worked with NCPC on campaigns.

The majority of scams are perpetrated by overseas scammers. Such cases are difficult to investigate and prosecute as these scammers typically run sophisticated transnational operations and hide behind the anonymity provided by the Internet.

Solving these cases also depends on the level of cooperation from overseas law enforcement agencies, and their ability to track down the scammers in their jurisdiction.

A discerning public is the first line of defence against scams. We urge the public to always verify the authenticity of requests received.

Brenda Ong (Superintendent)

Assistant Director (Public Communications Division)

Public Affairs Department

Singapore Police Force

.

===========

.

OCBC phishing scam: Police say they rushed to take down fake bank websites, trace lost cash

Anti-Scam Division senior investigation officers (from left) ASP Lim Min Siang, ASP Felicia Seow and INSP Eric Low have worked on a variety of scam cases. (Photo: CNA/Calvin Oh)

28 Jan 2022 08:00PM(Updated: 28 Jan 2022 08:13PM) in channelnewsasia.com

SINGAPORE: Deputy Assistant Commissioner of Police (DAC) Aileen Yap remembers how in early December last year, reports on the OCBC SMS phishing scam started trickling in.

In that period, there were about one or two cases a day, said DAC Yap, assistant director of the Anti-Scam Division. Then in the days leading up to Christmas and beyond, the reports suddenly spiked.

“When all these reports came in, obviously there’ll be corresponding bank accounts (of victims),” Assistant Superintendent of Police (ASP) Lim Min Siang, a senior investigation officer in the division, told reporters during a briefing at the Anti-Scam Centre on Thursday (Jan 27).

“That’s where the sense-making deep dive has to be done. Considering that the reports just kept coming in, it’s basically a race against time.”

The police said on Dec 30 that at least S$8.5 million was lost in phishing scams involving SMSes impersonating OCBC that month, with at least 469 victims since Dec 1.

Between Dec 8 and Dec 17, 26 customers reported they had lost about S$140,000 to phishing scams, OCBC said. The attacks grew “aggressive” during the Christmas weekend, the bank said, with 186 customers losing about US$2.7 million from Dec 24 to Dec 26.

Victims received unsolicited SMSes purportedly from OCBC claiming that their accounts had issues, and that these issues needed to be resolved by clicking on a link.

They were redirected to fake bank websites that requested they key in their iBanking account log-in details. They then received actual notifications on unauthorised transactions in their accounts – which is when they found out they had been scammed.

ASP Lim Min Siang wants the public to know that once victims’ money goes out of Singapore, it is likely gone. (Photo: CNA/Calvin Oh)

ASP Lim said on Thursday that the priority for officers was to take down the phishing websites. The ongoing investigation into the OCBC scam is being handled by officers from the Criminal Investigation Department (CID).

“Basically for the scammer, it’s very easy, they cast the net (wide),” he said. “So the idea (for us) is to take down the link as fast as possible, and prevent such links from being activated again.”

The other urgent task was to trace the lost cash, he said, pointing out that the money will be routed through several accounts to evade detection.

“Once the funds go to X account, it will definitely go to Y and Z, so there’s also this race to trace it down and try to recover as much as possible,” he added. “Because once the money goes out (of Singapore), it’s usually very challenging to get it back.”

The police have successfully recovered cash that was transferred overseas, but this is not a guarantee, especially as some jurisdictions could require victims to go through complicated and expensive legal processes.

Assistant director of SPF’s Anti-Scam Division DAC Aileen Yap speaking to the media. (Photo: CNA/Calvin Oh)

Even if the money stays in Singapore, DAC Yap said tracing it is “not a very easy job”. She highlighted that scammers would break down the funds into smaller tranches, and distribute these across multiple bank accounts.

This is why a key strategy for the police is to freeze the bank accounts of suspected money mules as quickly as possible.

On Dec 26 last year, which was a Sunday, the police worked with the banks to trace the money lost in the OCBC scam, DAC Yap said, although she acknowledged that bank employees were not legally obliged to come into the office that day.

“You know, it’s Boxing Day after Christmas, so there are post-Christmas sales,” she said. “At the end of the day, everything (the banks did) was out of goodwill.”

An OCBC branch in Singapore. (File photo: iStock)

ASP Lim said the banks could also have their own challenges, and these could affect police investigations.

“Because if we want to have some information and they’re unable to give, or they take time to give, then that will also prolong the analysis and the investigation,” he said.

While DAC Yap said the local banks were committed in providing information and gave “a lot of support”, some of the money had gone elsewhere.

“So, that is when the lead sort of died. The information on where the money went to subsequently came in much later. By then, all the money would either be withdrawn already or went to other countries,” she said.

“Our role at that point of time is really on fund recovery, up till now also. But the entire investigation is still ongoing. (We are) not giving up yet, because we can see our CID colleagues working very hard on this.”

The Anti-Scam Centre in the Police Cantonment Complex is the police’s nerve centre for investigating scam-related crimes.. (Photo: CNA/Calvin Oh)

ASP Lim said officers definitely felt “overwhelmed” when the OCBC scam reports came flooding in, but stressed that they remained “professional”.

“We are away from our family, friends and what not. But we have a job to do, so we just do it to the best of our abilities and try to at least prevent more victims from suffering from scams, or the victims from suffering even more losses.”

Source: CNA/ic

.

===========

.

I have gone back to activating and using my manual token. It has been replaced two days ago at the bank branch.

However, I have noticed that the digital token system is still showing up in the accounts even though I have a new manual token.

.

======

.

Forum: Limit digital transactions to just one bank account

PUBLISHED 5 HOURS AGO on 26th Jan 2022 in ST Forum.

In their efforts to go digital, banks have used carrot-and-stick tactics to get their clients to convert to digital banking.

But the digital banking platform is often a one-size-fits-all system.

For example, on one local bank’s digital banking platform, I have no choice but to link all my bank accounts in that bank, including all joint accounts with my name on them. I can perform any digital banking transaction on any of my bank accounts using my smartphone with the same login information. This is dangerous.

The recent phishing scams targeting OCBC Bank customers show that scammers can empty out victims’ accounts in no time. Other settings can also be changed by scammers who have access to the online banking accounts.

Many people do not need to have digital access to their entire savings.

To prevent massive loss of money through digital fraud, the Monetary Authority of Singapore should make it a requirement for banks to have account holders designate only one bank account from which they can make digital payments.

Account holders should also be encouraged to keep only a small amount of money sufficient for short-term expenditure in this account.

They should be encouraged to place the rest of their savings in a separate bank account which does not allow any digital transactions.

Should an account holder need to move funds between a savings account and a digital payment account, he should be required to do it in person at an ATM or bank branch.

This would limit the amount of money lost should the account holder fall victim to a scam. Wealthier depositors could opt to open multiple bank accounts from which they could make digital payments.

Lim Chong Teck.

.

=======

.

‘It was like fighting a war’: OCBC group CEO on dealing with recent phishing scams

OCBC group chief executive Helen Wong said the decision to pay all customers their losses as a gesture of goodwill was made in early January and the bank has been doing so since Jan 8.ST PHOTO: JASON QUAH

“It was like fighting a war,” said OCBC group chief executive Helen Wong of the massive phishing scam that hit the bank.

The war escalated quickly as deposits drained from compromised bank accounts, even as bank staff scrambled to shut down transfers to mule accounts. “As we blocked the mule accounts, the fraudsters somehow managed to find new mule accounts for the money to be paid into,” said Ms Wong, in an exclusive interview with The Straits Times.

Describing the attacks which took place as “fast and furious” and well-strategised, she said some funds were immediately remitted overseas as the scammers had fraudulently added new payees abroad.

When the first phishing scams surfaced in early December at OCBC, there were only a few cases, but a team in the bank was already investigating this, said Ms Wong on Friday.

On Dec 3, the bank posted a security advisory on its website, warning customers of the phishing attacks. As more phishing websites were detected, the bank’s anti-fraud team alerted domain providers to take them down.

Further warnings were issued to customers, but the situation worsened in the days leading up to Christmas. The bank knew it had a crisis on its hands.

The fraudsters had picked a clever time to attack, when people were winding down for the Christmas holidays, with some victims travelling overseas and not paying attention to their accounts, said Ms Wong.

OCBC issued text messages and pushed alerts to its one million customers to warn them of the attacks. A media advisory was also issued on Dec 23.

But over the Christmas weekend, another 186 customers fell prey, losing about $2.7 million.

<p>An SMS scam sms from ‘OCBC’ bank. </p>PHOTO: JOYCE FANG

While the bank’s front-line staff tended to victims, much more was going on behind the scenes to manage the crisis.

By Christmas, more than 100 people were working to fight the scams, operating round the clock.

Staff from various departments including fraud risk, and operations and technology teams, were deployed. Leave was cancelled and staff were recalled. Some who had retired were asked to come back to help, said Ms Wong.

Besides working to detect and stop the fraudulent transactions, there were staff who spent whole days just trawling through clients’ portfolios to check if there were any suspicious transactions, said Ms Wong, who meets her top management team every day.

With all hands on deck, the anti-fraud team managed to detect and stop suspicious transactions in more than 200 customers’ accounts.

“Some customers did not even know that their accounts had been hacked when our officers called them,” she said, adding that the team also managed to trace and recover some of the lost amounts. She did not reveal further details on this.

The bank’s hotline was jammed as worried customers called to make inquiries even though they did not receive the phishing messages. The volume of calls to the bank surged by 40 per cent, she said.

Staff from other departments were also deployed to help the call centre. Even so, some customers were unable to reach the bank in time.

“We feel very sorry about it, that they could not reach us promptly to report the scams. They do expect quick answers and assistance to stop the transactions that were occurring. And we fell short of their expectations and our own service standard,” said Ms Wong.

Apologising repeatedly during the interview at OCBC Centre, she said: “This truly bothers me. I feel truly sorry for the victims, and OCBC can and will do better. This is very important.”

Ms Wong, 60, became the first female chief executive to head a Singapore bank when she took over from Mr Samuel Tsien in April last year. The veteran banker was formerly the chief executive of HSBC in Greater China.

She said the decision to pay all customers their losses as a gesture of goodwill was made early this month, and the bank had been doing so since Jan 8.